| ☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

| ☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

Michigan

|

38-3391345

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common Stock

|

The Nasdaq Stock Market

|

|

Large accelerated filer ☐

|

Accelerated filer ☒

|

Non-accelerated filer ☐

|

Smaller reporting company ☒

|

Emerging growth company ☐

|

|

PART 1

|

Page

|

|

|

Item 1:

|

1

|

|

|

Item 1A:

|

12

|

|

|

Item 1B:

|

20

|

|

|

Item 2:

|

20 | |

|

Item 3:

|

20 | |

|

Item 4:

|

20 | |

|

PART II

|

||

|

Item 5:

|

21 | |

|

Item 6:

|

23

|

|

|

Item 7:

|

24

|

|

|

Item 7A:

|

41 | |

|

Item 8:

|

43 | |

|

Item 9:

|

84 | |

|

Item 9A:

|

84 | |

|

Item 9B:

|

86 | |

|

PART III

|

||

|

Item 10:

|

86 | |

|

Item 11:

|

86 | |

|

Item 12:

|

86 | |

|

Item 13:

|

86 | |

|

Item 14:

|

86

|

|

|

PART IV

|

||

|

Item 15:

|

87

|

|

|

Item 16:

|

87

|

|

|

88

|

|

December 31,

|

||||||||||||

|

(Dollars in thousands)

|

2018

|

2017

|

2016

|

|||||||||

|

Nonperforming loans

|

$

|

1,304

|

$

|

395

|

$

|

300

|

||||||

|

Other repossessed assets

|

—

|

11

|

—

|

|||||||||

|

Other real estate owned

|

3,380

|

5,767

|

12,253

|

|||||||||

|

Total nonperforming assets

|

$

|

4,684

|

$

|

6,173

|

$

|

12,553

|

||||||

|

Total delinquencies 30 days or greater past due

|

$

|

877

|

$

|

995

|

$

|

1,447

|

||||||

|

For the Year Ended December 31,

|

|||||||||||||

|

(Dollars in thousands)

|

2018

|

2017

|

2016

|

||||||||||

|

Provision for loan losses

|

$

|

450

|

$

|

(1,350)

|

|

$

|

(1,350)

|

|

|||||

|

Net charge-offs (recoveries)

|

174

|

(988)

|

|

(1,231)

|

|

||||||||

|

Net charge-offs (recoveries) to average loans

|

0.01

|

%

|

(0.08)

|

% |

(0.10)

|

% | |

||||||

|

Nonperforming loans to total loans

|

0.09

|

%

|

0.03

|

% |

0.02

|

% | |

||||||

|

Loans transferred to ORE to average loans

|

0.02

|

%

|

0.01

|

% |

0.03

|

% | |

||||||

|

Performing troubled debt restructurings (“TDRs”) to average loans

|

1.20

|

%

|

1.72

|

% |

2.45

|

% | |

||||||

|

December 31

|

||||||||||||||||||||||||||||||||||||||||

|

2018

|

2017

|

2016

|

2015

|

2014

|

||||||||||||||||||||||||||||||||||||

|

(Dollars in thousands)

|

Amount

|

% of

Total

Loans

|

Amount

|

% of

Total

Loans

|

Amount

|

% of

Total

Loans

|

Amount

|

% of

Total

Loans

|

Amount

|

% of

Total

Loans

|

||||||||||||||||||||||||||||||

|

Real estate - construction (1)

|

$

|

81,963

|

6

|

%

|

$

|

78,487

|

6

|

%

|

$

|

64,968

|

5

|

%

|

$

|

90,039

|

7

|

%

|

$

|

77,564

|

7

|

%

|

||||||||||||||||||||

|

Real estate - mortgage

|

486,748

|

35

|

463,448

|

35

|

453,013

|

35

|

418,633

|

35

|

412,967

|

37

|

||||||||||||||||||||||||||||||

|

Commercial and industrial

|

513,345

|

36

|

465,208

|

35

|

449,342

|

35

|

377,298

|

31

|

327,674

|

29

|

||||||||||||||||||||||||||||||

|

Total commercial

|

1,082,056

|

77

|

1,007,143

|

76

|

967,323

|

76

|

885,970

|

73

|

818,205

|

73

|

||||||||||||||||||||||||||||||

|

Residential mortgage

|

238,174

|

17

|

224,452

|

17

|

217,614

|

17

|

209,972

|

18

|

190,249

|

17

|

||||||||||||||||||||||||||||||

|

Consumer

|

85,428

|

6

|

88,714

|

7

|

95,875

|

7

|

101,990

|

9

|

110,029

|

10

|

||||||||||||||||||||||||||||||

|

Total loans

|

1,405,658

|

100

|

%

|

1,320,309

|

100

|

%

|

1,280,812

|

100

|

%

|

1,197,932

|

100

|

%

|

1,118,483

|

100

|

%

|

|||||||||||||||||||||||||

|

Less: allowance for loan losses

|

(16,876

|

)

|

(16,600

|

)

|

(16,962

|

)

|

(17,081

|

)

|

(18,962

|

)

|

||||||||||||||||||||||||||||||

|

Total loans, net

|

$

|

1,388,782

|

$

|

1,303,709

|

$

|

1,263,850

|

$

|

1,180,851

|

$

|

1,099,521

|

||||||||||||||||||||||||||||||

| (1) |

Consists of construction and development loans.

|

|

Maturing

|

||||||||||||||||

|

(Dollars in thousands)

|

Within One

Year

|

After One,

But

Within Five

Years

|

After Five

Years

|

Total

|

||||||||||||

|

Real estate - construction (1)

|

$

|

25,713

|

$

|

37,176

|

$

|

19,074

|

$

|

81,963

|

||||||||

|

Real estate - mortgage

|

48,937

|

312,054

|

125,757

|

486,748

|

||||||||||||

|

Commercial and industrial

|

293,866

|

195,223

|

24,256

|

513,345

|

||||||||||||

|

Total commercial

|

368,516

|

544,453

|

169,087

|

1,082,056

|

||||||||||||

|

Residential mortgage

|

184

|

5,331

|

232,659

|

238,174

|

||||||||||||

|

Consumer

|

2,117

|

19,752

|

63,559

|

85,428

|

||||||||||||

|

Total loans

|

$

|

370,817

|

$

|

569,536

|

$

|

465,305

|

$

|

1,405,658

|

||||||||

|

Maturing or Repricing

|

||||||||||||||||

|

Loans above:

|

||||||||||||||||

|

With predetermined interest rates

|

$

|

109,341

|

$

|

412,507

|

$

|

140,556

|

$

|

662,404

|

||||||||

|

With floating or adjustable rates

|

619,207

|

69,048

|

53,695

|

741,950

|

||||||||||||

|

Total (excluding nonaccrual loans)

|

$

|

728,548

|

$

|

481,555

|

$

|

194,251

|

1,404,354

|

|||||||||

|

Nonaccrual loans

|

1,304

|

|||||||||||||||

|

Total loans

|

$

|

1,405,658

|

||||||||||||||

| (1) |

Consists of construction and development loans.

|

|

December 31

|

||||||||||||||||||||||||

|

2018

|

2017

|

2016

|

||||||||||||||||||||||

|

(Dollars in thousands)

|

Average

Amount

|

Average

Rate

|

Average

Amount

|

Average

Rate

|

Average

Amount

|

Average

Rate

|

||||||||||||||||||

|

Noninterest bearing demand

|

$

|

467,663

|

---

|

%

|

$

|

464,384

|

---

|

%

|

$

|

445,046

|

---

|

%

|

||||||||||||

|

Interest bearing demand

|

406,694

|

0.3

|

341,384

|

0.1

|

321,825

|

0.1

|

||||||||||||||||||

|

Savings and money market accounts

|

602,676

|

0.6

|

557,703

|

0.3

|

521,857

|

0.2

|

||||||||||||||||||

|

Time

|

109,715

|

1.3

|

85,921

|

0.8

|

84,170

|

0.6

|

||||||||||||||||||

|

Total deposits

|

$

|

1,586,748

|

0.5

|

%

|

$

|

1,449,392

|

0.3

|

%

|

$

|

1,372,898

|

0.1

|

%

|

||||||||||||

|

Three months or less

|

$

|

17,327

|

||

|

Over 3 months through 6 months

|

11,496

|

|||

|

Over 6 months through 1 year

|

21,485

|

|||

|

Over 1 year

|

20,797

|

|||

|

$

|

71,105

|

|

December 31,

|

||||||||||||

|

(Dollars in thousands)

|

2018

|

2017

|

2016

|

|||||||||

|

U.S. Treasury and federal agency securities

|

$

|

95,398

|

$

|

101,964

|

$

|

84,350

|

||||||

|

U.S. Agency MBS and CMOs

|

32,890

|

23,385

|

11,817

|

|||||||||

|

Tax-exempt state and municipal bonds

|

115,461

|

127,884

|

108,565

|

|||||||||

|

Taxable state and municipal bonds

|

45,934

|

43,735

|

33,883

|

|||||||||

|

Corporate bonds

|

7,637

|

8,109

|

13,726

|

|||||||||

|

Other equity securities

|

—

|

1,470

|

1,470

|

|||||||||

|

Total

|

$

|

297,320

|

$

|

306,547

|

$

|

253,811

|

||||||

|

Due Within One Year

|

One to Five Years

|

Five to Ten Years

|

After Ten Years

|

|||||||||||||||||||||||||||||

|

(Dollars in thousands)

|

Amount

|

Average

Yield

|

Amount

|

Average

Yield

|

Amount

|

Average

Yield

|

Amount

|

Average

Yield

|

||||||||||||||||||||||||

|

U.S. Treasury and federal agency securities

|

$

|

14,647

|

1.44

|

%

|

$

|

77,774

|

1.92

|

%

|

$

|

2,978

|

2.77

|

%

|

$

|

—

|

—

|

%

|

||||||||||||||||

|

U.S. Agency MBS and CMOs

|

—

|

—

|

267

|

2.28

|

1,774

|

2.73

|

30,849

|

2.64

|

||||||||||||||||||||||||

|

Tax-exempt state and municipal bonds (1)

|

8,657

|

1.92

|

43,032

|

3.29

|

44,132

|

3.10

|

19,640

|

2.74

|

||||||||||||||||||||||||

|

Taxable state and municipal bonds

|

5,962

|

2.04

|

32,958

|

2.28

|

5,928

|

2.92

|

1,086

|

2.25

|

||||||||||||||||||||||||

|

Corporate bonds

|

3,064

|

2.05

|

4,572

|

1.35

|

—

|

—

|

—

|

—

|

||||||||||||||||||||||||

|

Total (1)

|

$

|

32,330

|

1.73

|

%

|

$

|

158,603

|

2.37

|

%

|

$

|

54,812

|

3.05

|

%

|

$

|

51,575

|

2.62

|

%

|

||||||||||||||||

| (1) |

Yields on tax-exempt securities are computed on a fully taxable-equivalent basis.

|

|

CET1 Risk-Based

Capital Ratio

|

Tier 1 Risk-Based

Capital Ratio

|

Total Risk-Based

Capital Ratio

|

Leverage Ratio

|

|||||

|

Well capitalized

|

6.5% or above

|

8% or above

|

10% or above

|

5% or above

|

||||

|

Adequately capitalized

|

4.5% or above

|

6% or above

|

8% or above

|

4% or above

|

||||

|

Undercapitalized

|

Less than 4.5%

|

Less than 6%

|

Less than 8%

|

Less than 4%

|

||||

|

Significantly undercapitalized

|

Less than 3%

|

Less than 4%

|

Less than 6%

|

Less than 3%

|

||||

|

Critically undercapitalized

|

—

|

—

|

—

|

Ratio of tangible equity to total assets of 2% or less

|

| · |

Variations in our anticipated or actual operating results or the results of our competitors;

|

| · |

Changes in investors’ or analysts’ perceptions of the risks and conditions of our business;

|

| · |

The size of the public float of our common stock;

|

| · |

Regulatory developments, including changes to regulatory capital levels, components of regulatory capital and how regulatory capital is calculated;

|

| · |

Interest rate changes or credit loss trends;

|

| · |

Trading volume in our common stock;

|

| · |

Market conditions; and

|

| · |

General economic conditions.

|

|

Location of Facility

|

Use

|

|

10753 Macatawa Drive, Holland

|

Main Branch, Administrative, and Loan Processing Offices

|

|

815 E. Main Street, Zeeland

|

Branch Office

|

|

116 Ottawa Avenue N.W., Grand Rapids

|

Branch Office (Leased facility, lease expires August 2020)

|

|

126 Ottawa Avenue N.W., Grand Rapids

|

Loan Center (Leased facility, lease expires August 2020)

|

|

141 E. 8th Street, Holland

|

Branch Office

|

|

489 Butternut Dr., Holland

|

Branch Office

|

|

701 Maple Avenue, Holland

|

Branch Office

|

|

699 E. 16th Street, Holland

|

Branch Office

|

|

41 N. State Street, Zeeland

|

Branch Office

|

|

2020 Baldwin Street, Jenison

|

Branch Office

|

|

6299 Lake Michigan Dr., Allendale

|

Branch Office

|

|

132 South Washington, Douglas

|

Branch Office

|

|

4758 – 136th Street, Hamilton

|

Branch Office (Leased facility, lease expires December 2019)

|

|

3526 Chicago Drive, Hudsonville

|

Branch Office

|

|

20 E. Lakewood Blvd., Holland

|

Branch Office

|

|

3191 – 44th Street, S.W., Grandville

|

Branch Office

|

|

2261 Byron Center Avenue S.W., Byron Center

|

Branch Office

|

|

5271 Clyde Park Avenue, S.W., Wyoming

|

Branch Office and Loan Center

|

|

4590 Cascade Road, Grand Rapids

|

Branch Office

|

|

3177 Knapp Street, N.E., Grand Rapids

|

Branch Office and Loan Center

|

|

15135 Whittaker Way, Grand Haven

|

Branch Office

|

|

12415 Riley Street, Holland

|

Branch Office

|

|

2750 Walker N.W., Walker

|

Branch Office

|

|

1575 – 68th Street S.E., Grand Rapids

|

Branch Office

|

|

2820 – 10 Mile Road, Rockford

|

Branch Office

|

|

520 Baldwin Street, Jenison

|

Branch Office

|

|

2440 Burton Street, S.E., Grand Rapids

|

Branch Office

|

|

6330 28 th Street, S.E., Grand Rapids

|

Branch Office

|

|

2018

|

2017

|

|||||||||||||||||||||||

|

Quarter

|

High

|

Low

|

Dividends

Declared

|

High

|

Low

|

Dividends

Declared

|

||||||||||||||||||

|

First Quarter

|

$

|

10.63

|

$

|

9.75

|

$

|

0.06

|

$

|

10.31

|

$

|

9.61

|

$

|

0.04

|

||||||||||||

|

Second Quarter

|

12.77

|

10.30

|

0.06

|

10.41

|

9.15

|

0.04

|

||||||||||||||||||

|

Third Quarter

|

12.77

|

11.64

|

0.06

|

10.40

|

9.14

|

0.05

|

||||||||||||||||||

|

Fourth Quarter

|

11.59

|

9.15

|

0.07

|

10.57

|

9.66

|

0.05

|

||||||||||||||||||

|

Period Ending

|

||||||||||||||||||||||||

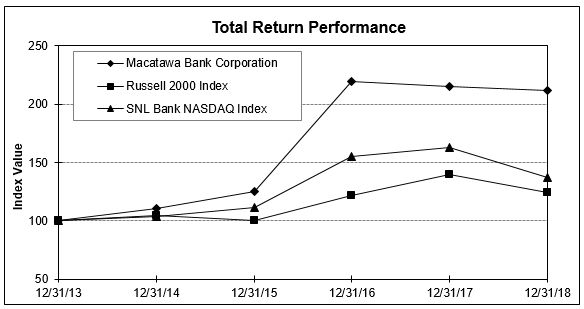

|

Index

|

12/31/13

|

12/31/14

|

12/31/15

|

12/31/16

|

12/31/17

|

12/31/18

|

||||||||||||||||||

|

Macatawa Bank Corporation

|

100.00

|

110.52

|

125.49

|

219.59

|

214.94

|

211.56

|

||||||||||||||||||

|

Russell 2000

|

100.00

|

104.89

|

100.26

|

121.63

|

139.44

|

124.09

|

||||||||||||||||||

|

SNL Bank NASDAQ

|

100.00

|

103.57

|

111.80

|

155.02

|

163.20

|

137.56

|

||||||||||||||||||

|

Macatawa Bank Corporation Purchases of Equity Securities

|

||||||||

|

Total

Number of

Shares

Purchased

|

Average

Price Paid

Per Share

|

|||||||

|

Period

|

||||||||

|

October 1 - October 31, 2018

|

||||||||

|

Employee Transactions

|

—

|

—

|

||||||

|

November 1 - November 30, 2018

|

||||||||

|

Employee Transactions

|

9,685

|

$

|

10.36

|

|||||

|

December 1 - December 31, 2018

|

||||||||

|

Employee Transactions

|

3,214

|

$

|

9.60

|

|||||

|

Total for Fourth Quarter ended December 31, 2018

|

||||||||

|

Employee Transactions

|

12,899

|

$

|

10.17

|

|||||

|

As of and for the Year Ended December 31,

|

||||||||||||||||||||

|

(Dollars in thousands, except per share data)

|

2018

|

2017

|

2016

|

2015

|

2014

|

|||||||||||||||

|

Financial Condition

|

||||||||||||||||||||

|

Total assets

|

$

|

1,975,124

|

$

|

1,890,232

|

$

|

1,741,013

|

$

|

1,729,643

|

$

|

1,583,846

|

||||||||||

|

Securities

|

297,320

|

306,547

|

253,811

|

218,671

|

193,459

|

|||||||||||||||

|

Loans

|

1,405,658

|

1,320,309

|

1,280,812

|

1,197,932

|

1,118,483

|

|||||||||||||||

|

Deposits

|

1,676,739

|

1,579,010

|

1,448,724

|

1,435,512

|

1,306,325

|

|||||||||||||||

|

Long-term debt

|

41,238

|

41,238

|

41,238

|

41,238

|

41,238

|

|||||||||||||||

|

Other borrowed funds

|

60,000

|

92,118

|

84,173

|

96,169

|

88,107

|

|||||||||||||||

|

Shareholders’ equity

|

190,853

|

172,986

|

162,239

|

151,977

|

142,519

|

|||||||||||||||

|

Share Information*

|

||||||||||||||||||||

|

Basic earnings (loss) per common share

|

$

|

0.78

|

$

|

0.48

|

$

|

0.47

|

$

|

0.38

|

$

|

0.31

|

||||||||||

|

Diluted earnings (loss) per common share

|

0.78

|

0.48

|

0.47

|

0.38

|

0.31

|

|||||||||||||||

|

Book value per common share

|

5.61

|

5.09

|

4.78

|

4.48

|

4.21

|

|||||||||||||||

|

Tangible book value per common share

|

5.61

|

5.09

|

4.78

|

4.48

|

4.21

|

|||||||||||||||

|

Dividends per common share

|

0.25

|

0.18

|

0.12

|

0.11

|

0.08

|

|||||||||||||||

|

Dividend payout ratio

|

32.05

|

%

|

37.50

|

%

|

25.53

|

%

|

28.95

|

%

|

25.81

|

%

|

||||||||||

|

Average dilutive common shares outstanding

|

34,018,554

|

33,952,872

|

33,922,548

|

33,891,429

|

33,803,030

|

|||||||||||||||

|

Common shares outstanding at period end

|

34,045,411

|

33,972,977

|

33,940,788

|

33,925,113

|

33,866,789

|

|||||||||||||||

|

Operations

|

||||||||||||||||||||

|

Interest income

|

$

|

69,037

|

$

|

57,676

|

$

|

52,499

|

$

|

49,386

|

$

|

46,988

|

||||||||||

|

Interest expense

|

9,411

|

5,732

|

4,959

|

5,306

|

5,596

|

|||||||||||||||

|

Net interest income

|

59,626

|

51,944

|

47,540

|

44,080

|

41,392

|

|||||||||||||||

|

Provision for loan losses

|

450

|

(1,350

|

)

|

(1,350

|

)

|

(3,500

|

)

|

(3,350

|

)

|

|||||||||||

|

Net interest income after provision for loan losses

|

59,176

|

53,294

|

48,890

|

47,580

|

44,742

|

|||||||||||||||

|

Total noninterest income

|

17,503

|

17,419

|

19,074

|

17,793

|

16,214

|

|||||||||||||||

|

Total noninterest expense

|

44,329

|

43,688

|

45,782

|

46,953

|

45,910

|

|||||||||||||||

|

Income before income tax

|

32,350

|

27,025

|

22,182

|

18,420

|

15,046

|

|||||||||||||||

|

Federal income tax**

|

5,971

|

10,733

|

6,231

|

5,626

|

4,573

|

|||||||||||||||

|

Net income attributable to common shares

|

26,379

|

16,292

|

15,951

|

12,794

|

10,473

|

|||||||||||||||

|

Performance Ratios

|

||||||||||||||||||||

|

Return on average equity

|

14.69

|

%

|

9.60

|

%

|

10.06

|

%

|

8.68

|

%

|

7.58

|

%

|

||||||||||

|

Return on average assets

|

1.40

|

0.93

|

0.95

|

0.79

|

0.70

|

|||||||||||||||

|

Yield on average interest-earning assets

|

3.91

|

3.59

|

3.42

|

3.36

|

3.48

|

|||||||||||||||

|

Cost on average interest-bearing liabilities

|

0.76

|

0.51

|

0.46

|

0.49

|

0.56

|

|||||||||||||||

|

Average net interest spread

|

3.15

|

3.08

|

2.96

|

2.87

|

2.92

|

|||||||||||||||

|

Average net interest margin

|

3.38

|

3.24

|

3.11

|

3.01

|

3.07

|

|||||||||||||||

|

Efficiency ratio

|

57.47

|

62.98

|

68.73

|

75.89

|

79.70

|

|||||||||||||||

|

Capital Ratios

|

||||||||||||||||||||

|

Period-end equity to total assets

|

9.66

|

%

|

9.15

|

%

|

9.32

|

%

|

8.79

|

%

|

9.00

|

%

|

||||||||||

|

Average equity to average assets

|

9.51

|

9.69

|

9.47

|

9.10

|

9.25

|

|||||||||||||||

|

Total risk-based capital ratio (consolidated)

|

15.54

|

14.99

|

14.88

|

14.80

|

15.55

|

|||||||||||||||

|

Credit Quality Ratios

|

||||||||||||||||||||

|

Allowance for loan losses to total loans

|

1.20

|

%

|

1.26

|

%

|

1.32

|

%

|

1.43

|

%

|

1.70

|

%

|

||||||||||

|

Nonperforming assets to total assets

|

0.24

|

0.33

|

0.72

|

1.06

|

2.32

|

|||||||||||||||

|

Net charge-offs / (recoveries) to average loans

|

0.01

|

(0.08

|

)

|

(0.10

|

)

|

(0.14

|

)

|

(0.14

|

)

|

|||||||||||

|

(Dollars in thousands)

|

December 31,

2018

|

December 31,

2017

|

December 31,

2016

|

|||||||||

|

Nonperforming loans

|

$

|

1,304

|

$

|

395

|

$

|

300

|

||||||

|

Other repossessed assets

|

—

|

11

|

—

|

|||||||||

|

Other real estate owned

|

3,380

|

5,767

|

12,253

|

|||||||||

|

Total nonperforming assets

|

$

|

4,684

|

$

|

6,173

|

$

|

12,553

|

||||||

|

Total loan delinquencies 30 days or greater past due

|

$

|

877

|

$

|

995

|

$

|

1,447

|

||||||

|

For the year ended December 31,

|

||||||||||||

|

(Dollars in thousands)

|

2018

|

2017

|

2016

|

|||||||||

|

Provision for loan losses

|

$

|

450

|

$

|

(1,350

|

)

|

$

|

(1,350

|

)

|

||||

|

Net charge-offs / (recoveries)

|

174

|

(988

|

)

|

(1,231

|

)

|

|||||||

|

Net charge-offs to average loans

|

0.01

|

%

|

-0.08

|

%

|

-0.10

|

%

|

||||||

|

Nonperforming loans to total loans

|

0.09

|

%

|

0.03

|

%

|

0.02

|

%

|

||||||

|

Loans transferred to ORE to average loans

|

0.02

|

%

|

0.01

|

%

|

0.01

|

%

|

||||||

|

Performing troubled debt restructurings to average loans

|

1.20

|

%

|

1.72

|

%

|

2.45

|

%

|

||||||

|

For the years ended December 31,

|

||||||||||||||||||||||||||||||||||||

|

2018

|

2017

|

2016

|

||||||||||||||||||||||||||||||||||

|

Average

Balance

|

Interest

Earned

or Paid

|

Average

Yield

or Cost

|

Average

Balance

|

Interest

Earned

or Paid

|

Average

Yield

or Cost

|

Average

Balance

|

Interest

Earned

or Paid

|

Average

Yield

or Cost

|

||||||||||||||||||||||||||||

|

Assets

|

||||||||||||||||||||||||||||||||||||

|

Taxable securities

|

$

|

180,787

|

$

|

3,716

|

2.06

|

%

|

$

|

158,805

|

$

|

2,869

|

1.81

|

%

|

$

|

136,051

|

$

|

2,322

|

1.71

|

%

|

||||||||||||||||||

|

Tax-exempt securities (1)

|

123,923

|

3,464

|

3.60

|

105,460

|

2,244

|

3.38

|

89,442

|

1,819

|

3.25

|

|||||||||||||||||||||||||||

|

Commercial loans (2)

|

1,012,413

|

46,369

|

4.52

|

957,987

|

39,658

|

4.08

|

906,506

|

35,946

|

3.90

|

|||||||||||||||||||||||||||

|

Residential mortgage loans

|

235,378

|

8,399

|

3.57

|

219,111

|

7,608

|

3.46

|

217,776

|

7,647

|

3.51

|

|||||||||||||||||||||||||||

|

Consumer loans

|

85,175

|

4,084

|

4.79

|

90,565

|

3,802

|

4.20

|

96,616

|

3,806

|

3.94

|

|||||||||||||||||||||||||||

|

Federal Home Loan Bank stock

|

11,558

|

578

|

4.94

|

11,558

|

491

|

4.19

|

11,558

|

491

|

4.18

|

|||||||||||||||||||||||||||

|

Federal funds sold and other short-term investments

|

124,374

|

2,427

|

1.92

|

83,844

|

1,004

|

1.18

|

90,243

|

468

|

0.51

|

|||||||||||||||||||||||||||

|

Total interest earning assets (1)

|

1,773,608

|

69,037

|

3.91

|

1,627,330

|

57,676

|

3.59

|

1,548,192

|

52,499

|

3.42

|

|||||||||||||||||||||||||||

|

Noninterest earning assets:

|

||||||||||||||||||||||||||||||||||||

|

Cash and due from banks

|

31,025

|

29,077

|

26,593

|

|||||||||||||||||||||||||||||||||

|

Other

|

83,808

|

95,896

|

98,799

|

|||||||||||||||||||||||||||||||||

|

Total assets

|

$

|

1,888,441

|

$

|

1,752,303

|

$

|

1,673,584

|

||||||||||||||||||||||||||||||

|

Liabilities

|

||||||||||||||||||||||||||||||||||||

|

Deposits:

|

||||||||||||||||||||||||||||||||||||

|

Interest bearing demand

|

$

|

406,694

|

$

|

1,130

|

0.28

|

%

|

$

|

341,384

|

$

|

366

|

0.11

|

%

|

$

|

321,825

|

$

|

293

|

0.09

|

%

|

||||||||||||||||||

|

Savings and money market accounts

|

602,676

|

3,317

|

0.55

|

557,703

|

1,591

|

0.28

|

521,857

|

961

|

0.19

|

|||||||||||||||||||||||||||

|

Time deposits

|

109,715

|

1,434

|

1.30

|

85,921

|

654

|

0.76

|

84,170

|

517

|

0.62

|

|||||||||||||||||||||||||||

|

Borrowings:

|

||||||||||||||||||||||||||||||||||||

|

Other borrowed funds

|

74,751

|

1,403

|

1.85

|

85,893

|

1,407

|

1.62

|

94,264

|

1,685

|

1.76

|

|||||||||||||||||||||||||||

|

Long-term debt

|

41,238

|

2,127

|

5.09

|

41,238

|

1,714

|

4.10

|

41,238

|

1,503

|

3.59

|

|||||||||||||||||||||||||||

|

Total interest bearing liabilities

|

1,235,074

|

9,411

|

0.76

|

1,112,139

|

5,732

|

0.51

|

1,063,354

|

4,959

|

0.46

|

|||||||||||||||||||||||||||

|

Noninterest bearing liabilities:

|

||||||||||||||||||||||||||||||||||||

|

Noninterest bearing demand accounts

|

467,663

|

464,384

|

445,046

|

|||||||||||||||||||||||||||||||||

|

Other noninterest bearing liabilities

|

6,077

|

6,004

|

6,618

|

|||||||||||||||||||||||||||||||||

|

Shareholders’ equity

|

179,627

|

169,776

|

158,566

|

|||||||||||||||||||||||||||||||||

|

Total liabilities and shareholders’ equity

|

$

|

1,888,441

|

$

|

1,752,303

|

$

|

1,673,584

|

||||||||||||||||||||||||||||||

|

Net interest income

|

$

|

59,626

|

$

|

51,944

|

$

|

47,540

|

||||||||||||||||||||||||||||||

|

Net interest spread (1)

|

3.15

|

%

|

3.08

|

%

|

2.96

|

%

|

||||||||||||||||||||||||||||||

|

Net interest margin (1)

|

3.38

|

%

|

3.24

|

%

|

3.11

|

%

|

||||||||||||||||||||||||||||||

|

Ratio of average interest earning assets to average interest bearing liabilities

|

143.60

|

%

|

146.32

|

%

|

145.60

|

%

|

||||||||||||||||||||||||||||||

| (1) |

Yields are presented on a tax equivalent basis using a 21% tax rate for 2018 and a 35% tax rate for 2017 and 2016.

|

| (2) |

Loan fees of $701,000, $701,000 and $883,000 for 2018, 2017 and 2016, respectively, are included in interest income. Includes average nonaccrual loans of approximately

$316,000, $492,000 and $372,000 for 2018, 2017 and 2016, respectively.

|

|

For the years ended December 31,

|

||||||||||||||||||||||||

|

2018 vs 2017

Increase (Decrease) Due to

|

2017 vs 2016

Increase (Decrease) Due to

|

|||||||||||||||||||||||

|

Volume

|

Rate

|

Total

|

Volume

|

Rate

|

Total

|

|||||||||||||||||||

|

(Dollars in thousands)

|

||||||||||||||||||||||||

|

Interest income

|

||||||||||||||||||||||||

|

Taxable securities

|

$

|

425

|

$

|

422

|

$

|

847

|

$

|

405

|

$

|

142

|

$

|

547

|

||||||||||||

|

Tax-exempt securities

|

834

|

386

|

1,220

|

338

|

87

|

425

|

||||||||||||||||||

|

Commercial loans

|

2,337

|

4,374

|

6,711

|

2,092

|

1,620

|

3,712

|

||||||||||||||||||

|

Residential mortgage loans

|

576

|

215

|

791

|

46

|

(85

|

)

|

(39

|

)

|

||||||||||||||||

|

Consumer loans

|

(236

|

)

|

518

|

282

|

(243

|

)

|

239

|

(4

|

)

|

|||||||||||||||

|

Federal Home Loan Bank stock

|

—

|

87

|

87

|

—

|

—

|

—

|

||||||||||||||||||

|

Federal funds sold and other short-term investments

|

618

|

805

|

1,423

|

(35

|

)

|

571

|

536

|

|||||||||||||||||

|

Total interest income

|

4,554

|

6,807

|

11,361

|

2,603

|

2,574

|

5,177

|

||||||||||||||||||

|

Interest expense

|

||||||||||||||||||||||||

|

Interest bearing demand

|

$

|

82

|

$

|

682

|

$

|

764

|

$

|

19

|

$

|

54

|

$

|

73

|

||||||||||||

|

Savings and money market accounts

|

138

|

1,588

|

1,726

|

70

|

560

|

630

|

||||||||||||||||||

|

Time deposits

|

217

|

563

|

780

|

11

|

126

|

137

|

||||||||||||||||||

|

Other borrowed funds

|

(192

|

)

|

188

|

(4

|

)

|

(143

|

)

|

(135

|

)

|

(278

|

)

|

|||||||||||||

|

Long-term debt

|

—

|

413

|

413

|

—

|

211

|

211

|

||||||||||||||||||

|

Total interest expense

|

245

|

3,434

|

3,679

|

(43

|

)

|

816

|

773

|

|||||||||||||||||

|

Net interest income

|

$

|

4,309

|

$

|

3,373

|

$

|

7,682

|

$

|

2,646

|

$

|

1,758

|

$

|

4,404

|

||||||||||||

|

2018

|

2017

|

|||||||

|

Service charges and fees on deposit accounts

|

$

|

4,377

|

$

|

4,466

|

||||

|

Net gains on mortgage loans

|

924

|

1,574

|

||||||

|

Trust fees

|

3,643

|

3,277

|

||||||

|

Gain on sales of securities

|

—

|

3

|

||||||

|

ATM and debit card fees

|

5,535

|

5,207

|

||||||

|

Bank owned life insurance (“BOLI”) income

|

942

|

969

|

||||||

|

Investment services fees

|

989

|

910

|

||||||

|

Other income

|

1,093

|

1,013

|

||||||

|

Total noninterest income

|

$

|

17,503

|

$

|

17,419

|

||||

|

For the Year Ended December 31,

|

||||||||

|

2018

|

2017

|

|||||||

|

Gain on sales of loans

|

$

|

924

|

$

|

1,574

|

||||

|

Real estate mortgage loans originated for sale

|

$

|

33,907

|

$

|

56,985

|

||||

|

Real estate mortgage loans sold

|

35,624

|

59,532

|

||||||

|

Net gain on the sale of mortgage loans as a percent of real estate mortgage loans sold (“Loan sale

margin”)

|

2.59

|

%

|

2.64

|

%

|

||||

|

2018

|

2017

|

|||||||

|

Salaries and benefits

|

$

|

25,207

|

$

|

24,803

|

||||

|

Occupancy of premises

|

3,931

|

3,864

|

||||||

|

Furniture and equipment

|

3,125

|

3,050

|

||||||

|

Legal and professional

|

806

|

812

|

||||||

|

Marketing and promotion

|

881

|

882

|

||||||

|

Data processing

|

2,986

|

2,759

|

||||||

|

FDIC assessment

|

518

|

539

|

||||||

|

Interchange and other card expense

|

1,409

|

1,306

|

||||||

|

Bond and D&O insurance

|

440

|

471

|

||||||

|

Net (gains) losses on repossessed and foreclosed properties

|

(207

|

)

|

(428

|

)

|

||||

|

Administration and disposition of problem assets

|

276

|

493

|

||||||

|

Outside services

|

1,696

|

1,677

|

||||||

|

Other noninterest expense

|

3,261

|

3,460

|

||||||

|

Total noninterest expense

|

$

|

44,329

|

$

|

43,688

|

||||

|

2018

|

2017

|

|||||||

|

Legal and professional –

nonperforming assets

|

$

|

93

|

$

|

107

|

||||

|

Repossessed and foreclosed property administration

|

183

|

386

|

||||||

|

Net (gains) losses on repossessed and foreclosed properties

|

(207

|

)

|

(428

|

)

|

||||

|

Total

|

$

|

69

|

$

|

65

|

||||

|

December 31, 2018

|

December 31, 2017

|

|||||||||||||||

|

Balance

|

Percent of

Total Loans

|

Balance

|

Percent of

Total Loans

|

|||||||||||||

|

Commercial real estate: (1)

|

||||||||||||||||

|

Residential developed

|

$

|

14,825

|

1.1

|

%

|

$

|

11,888

|

0.9

|

%

|

||||||||

|

Unsecured to residential developers

|

—

|

—

|

2,332

|

0.2

|

||||||||||||

|

Vacant and unimproved

|

44,169

|

3.1

|

39,752

|

3.1

|

||||||||||||

|

Commercial development

|

712

|

0.1

|

1,103

|

—

|

||||||||||||

|

Residential improved

|

98,500

|

7.0

|

90,467

|

6.9

|

||||||||||||

|

Commercial improved

|

295,618

|

21.0

|

298,714

|

22.6

|

||||||||||||

|

Manufacturing and industrial

|

114,887

|

8.2

|

97,679

|

7.4

|

||||||||||||

|

Total commercial real estate

|

568,711

|

40.5

|

541,935

|

41.1

|

||||||||||||

|

Commercial and industrial

|

513,345

|

36.5

|

465,208

|

35.2

|

||||||||||||

|

Total commercial

|

1,082,056

|

77.0

|

1,007,143

|

76.3

|

||||||||||||

|

Consumer

|

||||||||||||||||

|

Residential mortgage

|

238,174

|

16.9

|

224,452

|

17.0

|

||||||||||||

|

Unsecured

|

130

|

—

|

226

|

—

|

||||||||||||

|

Home equity

|

78,503

|

5.6

|

82,234

|

6.2

|

||||||||||||

|

Other secured

|

6,795

|

0.5

|

6,254

|

0.5

|

||||||||||||

|

Total consumer

|

323,602

|

23.0

|

313,166

|

23.7

|

||||||||||||

|

Total loans

|

$

|

1,405,658

|

100.0

|

%

|

$

|

1,320,309

|

100.0

|

%

|

||||||||

| (1) |

Includes both owner occupied and non-owner occupied commercial real estate.

|

|

Year ended December 31, 2018

|

Year ended December 31, 2017

|

|||||||||||||||||||||||

|

Portfolio

Originations

|

Percent of

Total

Originations

|

Average

Loan Size

|

Portfolio

Originations

|

Percent of

Total

Originations

|

Average

Loan Size

|

|||||||||||||||||||

|

Commercial real estate:

|

||||||||||||||||||||||||

|

Residential developed

|

$

|

16,101

|

2.7

|

%

|

$

|

671

|

$

|

12,938

|

3.0

|

%

|

$

|

863

|

||||||||||||

|

Unsecured to residential developers

|

—

|

—

|

—

|

—

|

—

|

—

|

||||||||||||||||||

|

Vacant and unimproved

|

13,869

|

2.3

|

630

|

6,417

|

1.5

|

458

|

||||||||||||||||||

|

Commercial development

|

350

|

0.1

|

175

|

800

|

0.2

|

267

|

||||||||||||||||||

|

Residential improved

|

103,834

|

17.5

|

618

|

60,135

|

13.8

|

278

|

||||||||||||||||||

|

Commercial improved

|

41,634

|

7.0

|

706

|

87,319

|

20.0

|

1,164

|

||||||||||||||||||

|

Manufacturing and industrial

|

50,642

|

8.6

|

1,178

|

26,249

|

6.0

|

640

|

||||||||||||||||||

|

Total commercial real estate

|

226,430

|

38.2

|

712

|

193,858

|

44.5

|

533

|

||||||||||||||||||

|

Commercial and industrial

|

248,185

|

41.8

|

1,021

|

136,445

|

31.3

|

578

|

||||||||||||||||||

|

Total commercial

|

474,615

|

80.0

|

846

|

330,303

|

75.8

|

551

|

||||||||||||||||||

|

Consumer

|

||||||||||||||||||||||||

|

Residential mortgage

|

73,440

|

12.4

|

271

|

57,919

|

13.3

|

234

|

||||||||||||||||||

|

Unsecured

|

32

|

—

|

16

|

—

|

—

|

—

|

||||||||||||||||||

|

Home equity

|

41,357

|

7.0

|

88

|

45,076

|

10.4

|

85

|

||||||||||||||||||

|

Other secured

|

3,417

|

0.6

|

22

|

2,412

|

0.5

|

16

|

||||||||||||||||||

|

Total consumer

|

118,246

|

20.0

|

132

|

105,407

|

24.2

|

113

|

||||||||||||||||||

|

Total loans

|

$

|

592,861

|

100.0

|

%

|

407

|

$

|

435,710

|

100.0

|

%

|

284

|

||||||||||||||

|

December 31, 2018

|

December 31, 2017

|

|||||||||||||||||||||||

|

Foreclosed Asset Property

Type

|

Carrying

Value

|

Foreclosed

Asset

Writedown

|

Combined

Writedown

(Loan and

Foreclosed

Asset)

|

Carrying

Value

|

Foreclosed

Asset

Writedown

|

Combined

Writedown

(Loan and

Foreclosed

Asset)

|

||||||||||||||||||

|

Single Family

|

$

|

—

|

—

|

%

|

—

|

%

|

$

|

60

|

—

|

%

|

24.3

|

%

|

||||||||||||

|

Residential Lot

|

38

|

57.6

|

70.1

|

109

|

46.9

|

73.1

|

||||||||||||||||||

|

Multi-Family

|

—

|

—

|

—

|

—

|

—

|

—

|

||||||||||||||||||

|

Vacant Land

|

352

|

40.5

|

46.6

|

1,345

|

56.1

|

60.5

|

||||||||||||||||||

|

Residential Development

|

815

|

38.6

|

82.3

|

2,167

|

30.0

|

71.8

|

||||||||||||||||||

|

Commercial Office

|

—

|

—

|

—

|

—

|

—

|

—

|

||||||||||||||||||

|

Commercial Industrial

|

—

|

—

|

—

|

—

|

—

|

—

|

||||||||||||||||||

|

Commercial Improved

|

2,175

|

—

|

—

|

2,086

|

6.7

|

8.0

|

||||||||||||||||||

|

$

|

3,380

|

19.2

|

55.4

|

$

|

5,767

|

33.4

|

58.3

|

|||||||||||||||||

|

December 31,

|

||||||||||||||||||||

|

2018

|

2017

|

2016

|

2015

|

2014

|

||||||||||||||||

|

Nonaccrual loans

|

$

|

1,303

|

$

|

395

|

$

|

300

|

$

|

739

|

$

|

8,292

|

||||||||||

|

Loans 90 days or more delinquent and still accruing

|

1

|

—

|

—

|

17

|

134

|

|||||||||||||||

|

Total nonperforming loans (NPLs)

|

1,304

|

395

|

300

|

756

|

8,426

|

|||||||||||||||

|

Foreclosed assets

|

3,380

|

5,767

|

12,253

|

17,572

|

28,242

|

|||||||||||||||

|

Repossessed assets

|

—

|

11

|

—

|

—

|

38

|

|||||||||||||||

|

Total nonperforming assets (NPAs)

|

$

|

4,684

|

$

|

6,173

|

$

|

12,553

|

$

|

18,328

|

$

|

36,706

|

||||||||||

|

NPLs to total loans

|

0.09

|

%

|

0.03

|

%

|

0.02

|

%

|

0.06

|

%

|

0.75

|

%

|

||||||||||

|

NPAs to total assets

|

0.24

|

%

|

0.33

|

%

|

0.73

|

%

|

1.06

|

%

|

2.32

|

%

|

||||||||||

|

December 31, 2018

|

December 31, 2017

|

|||||||||||||||||||||||

|

Commercial

|

Consumer

|

Total

|

Commercial

|

Consumer

|

Total

|

|||||||||||||||||||

|

Performing TDRs

|

$

|

9,682

|

$

|

6,347

|

$

|

16,029

|

$

|

13,420

|

$

|

8,344

|

$

|

21,764

|

||||||||||||

|

Nonperforming TDRs (1)

|

124

|

—

|

124

|

315

|

1

|

316

|

||||||||||||||||||

|

Total TDRs

|

$

|

9,806

|

$

|

6,347

|

$

|

16,153

|

$

|

13,735

|

$

|

8,345

|

$

|

22,080

|

||||||||||||

| (1) |

Included in nonperforming asset table above

|

|

December 31,

|

||||||||||||||||||||

|

2018

|

2017

|

2016

|

2015

|

2014

|

||||||||||||||||

|

Commercial and industrial TDRs

|

$

|

6,502

|

$

|

6,403

|

$

|

5,994

|

$

|

7,611

|

$

|

9,085

|

||||||||||

|

Commercial real estate TDRs

|

3,305

|

7,332

|

11,933

|

17,871

|

29,817

|

|||||||||||||||

|

Consumer TDRs

|

6,346

|

8,345

|

12,059

|

13,570

|

14,495

|

|||||||||||||||

|

Total TDRs

|

$

|

16,153

|

$

|

22,080

|

$

|

29,986

|

$

|

39,052

|

$

|

53,397

|

||||||||||

|

December 31

|

||||||||||||||||||||

|

(Dollars in thousands)

|

2018

|

2017

|

2016

|

2015

|

2014

|

|||||||||||||||

|

Portfolio loans:

|

||||||||||||||||||||

|

Average daily balance of loans for the year

|

$

|

1,332,450

|

$

|

1,265,353

|

$

|

1,218,901

|

$

|

1,151,101

|

$

|

1,048,496

|

||||||||||

|

Amount of loans outstanding at end of period

|

1,405,658

|

1,320,309

|

1,280,812

|

1,197,932

|

1,118,483

|

|||||||||||||||

|

Allowance for loan losses:

|

||||||||||||||||||||

|

Balance at beginning of year

|

16,600

|

16,962

|

17,081

|

18,962

|

20,798

|

|||||||||||||||

|

Provision for loan losses

|

450

|

(1,350

|

)

|

(1,350

|

)

|

(3,500

|

)

|

(3,350

|

)

|

|||||||||||

|

Loans charged-off:

|

||||||||||||||||||||

|

Real estate - construction

|

—

|

—

|

—

|

—

|

-

|

|||||||||||||||

|

Real estate - mortgage

|

—

|

—

|

—

|

(218

|

)

|

(133

|

)

|

|||||||||||||

|

Commercial and industrial

|

(1,206

|

)

|

(108

|

)

|

—

|

(172

|

)

|

(43

|

)

|

|||||||||||

|

Total Commercial

|

(1,206

|

)

|

(108

|

)

|

—

|

(390

|

)

|

(176

|

)

|

|||||||||||

|

Residential mortgage

|

—

|

(19

|

)

|

(10

|

)

|

(158

|

)

|

(9

|

)

|

|||||||||||

|

Consumer

|

(129

|

)

|

(139

|

)

|

(195

|

)

|

(154

|

)

|

(491

|

)

|

||||||||||

|

(1,335

|

)

|

(266

|

)

|

(205

|

)

|

(702

|

)

|

(676

|

)

|

|||||||||||

|

Recoveries:

|

||||||||||||||||||||

|

Real estate - construction

|

238

|

333

|

426

|

699

|

869

|

|||||||||||||||

|

Real estate - mortgage

|

685

|

488

|

664

|

565

|

510

|

|||||||||||||||

|

Commercial and industrial

|

86

|

123

|

162

|

406

|

522

|

|||||||||||||||

|

Total Commercial

|

1,009

|

944

|

1,252

|

1,670

|

1,901

|

|||||||||||||||

|

Residential mortgage

|

55

|

66

|

33

|

415

|

142

|

|||||||||||||||

|

Consumer

|

97

|

244

|

151

|

236

|

147

|

|||||||||||||||

|

1,161

|

1,254

|

1,436

|

2,321

|

2,190

|

||||||||||||||||

|

Net (charge-offs) recoveries

|

(174

|

)

|

988

|

1,231

|

1,619

|

1,514

|

||||||||||||||

|

Balance at end of year

|

$

|

16,876

|

$

|

16,600

|

$

|

16,962

|

$

|

17,081

|

$

|

18,962

|

||||||||||

|

Ratios:

|

||||||||||||||||||||

|

Net charge-offs (recoveries) to average loans outstanding

|

0.01

|

%

|

(0.08

|

)%

|

(0.10

|

)%

|

(0.14

|

)%

|

(0.13

|

)%

|

||||||||||

|

Allowance for loan losses to loans outstanding at year-end

|

1.20

|

%

|

1.26

|

%

|

1.32

|

%

|

1.70

|

%

|

2.00

|

%

|

||||||||||

|

Allowance for loan losses to nonperforming loans at year-end

|

1,294.17

|

%

|

4,202.53

|

%

|

5,654.00

|

%

|

2,259.39

|

%

|

225.04

|

%

|

||||||||||

|

(Dollars in millions)

|

2018

|

2017

|

2016

|

2015

|

2014

|

|||||||||||||||

|

Commercial loans

|

$

|

1,082.1

|

$

|

1,007.1

|

$

|

967.3

|

$

|

886.0

|

$

|

818.2

|

||||||||||

|

Nonperforming loans

|

1.3

|

0.4

|

0.3

|

0.8

|

8.4

|

|||||||||||||||

|

Other real estate owned and repo assets

|

3.4

|

5.8

|

12.3

|

17.6

|

28.3

|

|||||||||||||||

|

Total nonperforming assets

|

4.7

|

6.2

|

12.6

|

18.3

|

36.7

|

|||||||||||||||

|

Net charge-offs (recoveries)

|

0.2

|

(1.0

|

)

|

(1.2

|

)

|

(1.6

|

)

|

(1.5

|

)

|

|||||||||||

|

Total delinquencies

|

0.9

|

1.0

|

1.4

|

1.4

|

2.8

|

|||||||||||||||

|

December 31,

|

||||||||||||||||||||||||||||||||||||||||

|

2018

|

2017

|

2016

|

2015

|

2014

|

||||||||||||||||||||||||||||||||||||

|

(Dollars in thousands)

|

Allowance

Amount

|

% of

Each

Category

to total

Loans

|

Allowance

Amount

|

% of

Each

Category

to total

Loans

|

Allowance

Amount

|

% of

Each

Category

to total

Loans

|

Allowance

Amount

|

% of

Each

Category

to total

Loans

|

Allowance

Amount

|

% of

Each

Category

to total

Loans

|

||||||||||||||||||||||||||||||

|

Commercial and commercial real estate

|

$

|

13,427

|

77

|

%

|

$

|

13,106

|

76

|

%

|

$

|

13,092

|

76

|

%

|

$

|

13,320

|

75

|

%

|

$

|

14,916

|

73

|

%

|

||||||||||||||||||||

|

Residential mortgage

|

2,477

|

17

|

2,508

|

17

|

2,646

|

17

|

2,557

|

17

|

2,689

|

17

|

||||||||||||||||||||||||||||||

|

Consumer

|

972

|

6

|

986

|

7

|

1,224

|

7

|

1,204

|

8

|

1,357

|

10

|

||||||||||||||||||||||||||||||

|

Total

|

$

|

16,876

|

100

|

%

|

$

|

16,600

|

100

|

%

|

$

|

16,962

|

100

|

%

|

$

|

17,081

|

100

|

%

|

$

|

18,962

|

100

|

%

|

||||||||||||||||||||

|

December 31,

|

||||||||||||||||

|

2018

|

2017

|

|||||||||||||||

|

(Dollars in thousands)

|

Balance of

Loans

|

Allowance

Amount

|

Balance of

Loans

|

Allowance

Amount

|

||||||||||||

|

Commercial and commercial real estate:

|

||||||||||||||||

|

Impaired with allowance recorded

|

$

|

7,541

|

$

|

630

|

$

|

10,091

|

$

|

694

|

||||||||

|

Impaired with no allowance recorded

|

3,333

|

—

|

3,643

|

—

|

||||||||||||

|

Loss allocation factor on non-impaired loans

|

1,071,182

|

12,797

|

993,409

|

12,412

|

||||||||||||

|

1,082,056

|

13,427

|

1,007,143

|

13,106

|

|||||||||||||

|

Residential mortgage and consumer:

|

||||||||||||||||

|

Reserves on troubled debt restructurings

|

6,347

|

468

|

8,345

|

514

|

||||||||||||

|

Loss allocation factor

|

317,255

|

2,981

|

304,821

|

2,980

|

||||||||||||

|

Total

|

$

|

1,405,658

|

$

|

16,876

|

$

|

1,320,309

|

$

|

16,600

|

||||||||

|

December 31,

|

||||||||||||

|

2018

|

2017

|

2016

|

||||||||||

|

Total capital to risk weighted assets

|

15.5

|

%

|

15.0

|

%

|

14.9

|

%

|

||||||

|

Common Equity Tier 1 to risk weighted assets

|

12.0

|

11.3

|

11.0

|

|||||||||

|

Tier 1 capital to risk weighted assets

|

14.5

|

13.9

|

13.7

|

|||||||||

|

Tier 1 capital to average assets

|

12.1

|

11.9

|

12.0

|

|||||||||

|

December 31,

|

||||||||||||

|

2018

|

2017

|

2016

|

||||||||||

|

Average equity to average assets

|

11.3

|

%

|

11.6

|

%

|

11.5

|

%

|

||||||

|

Total capital to risk weighted assets

|

15.1

|

14.6

|

14.5

|

|||||||||

|

Common Equity Tier 1 to risk weighted assets

|

14.1

|

13.5

|

13.4

|

|||||||||

|

Tier 1 capital to risk weighted assets

|

14.1

|

13.5

|

13.4

|

|||||||||

|

Tier 1 capital to average assets

|

11.8

|

11.6

|

11.7

|

|||||||||

|

Less than

1 year

|

1-3 years

|

3-5 years

|

More than

5 years

|

|||||||||||||

|

Long term debt

|

$

|

—

|

$

|

—

|

$

|

—

|

$

|

41,238

|

||||||||

|

Time deposit maturities

|

78,878

|

43,099

|

3,547

|

—

|

||||||||||||

|

Other borrowed funds

|

10,000

|

10,000

|

10,000

|

30,000

|

||||||||||||

|

Operating lease obligations

|

353

|

342

|

115

|

—

|

||||||||||||

|

Total

|

$

|

89,231

|

$

|

53,441

|

$

|

13,662

|

$

|

71,238

|

||||||||

|

Interest Rate

Scenario

|

Economic

Value of

Equity

|

Percent

Change

|

Net Interest

Income

|

Percent

Change

|

||||||||||||

|

Interest rates up 200 basis points

|

$

|

277,542

|

3.65

|

%

|

$

|

68,296

|

3.14

|

% | ||||||||

|

Interest rates up 100 basis points

|

283,437

|

(1.61

|

)

|

67,239

|

1.54

|

|||||||||||

|

No change

|

288,067

|

—

|

66,217

|

—

|

||||||||||||

|

Interest rates down 100 basis points

|

279,997

|

(2.80

|

)

|

64,931

|

(1.94

|

)

|

||||||||||

|

Interest rates down 200 basis points

|

259,451

|

(9.93

|

)

|

62,441

|

(5.70

|

)

|

||||||||||

|

2018

|

2017

|

|||||||

|

ASSETS

|

||||||||

|

Cash and due from banks

|

$

|

40,526

|

$

|

34,945

|

||||

|

Federal funds sold and other short-term investments

|

130,758

|

126,522

|

||||||

|

Cash and cash equivalents

|

171,284

|

161,467

|

||||||

|